Motoring / Advertising Feature

What amount can I save without stretching, and what date will that hit my target?

You can set a monthly saving amount that feels comfortable, then pinpoint the target date you reach your target amount for car finance. If you worry about a bad credit history, this step gives you control first: you build a deposit before speaking to any lender, which often improves your car finance options. When you feel ready, you can move on to our guidance on bad credit history to understand how lenders assess deposits, affordability, and recent payment behaviour.

You share your target amount and your monthly savings amount, and we lay out a simple timeline in clear figures. You see how many months it takes to reach your car finance deposit and the month you can start comparing finance options.

You stay in control of your budget from day one. You choose a monthly saving amount that leaves room for bills, food, fuel, and the costs that crop up, so your saving plan supports a car finance agreement you can maintain.

is needed now More than ever

What “saving without stretching” means

Saving without stretching means choosing a monthly saving amount you can keep paying without stress. You protect your core spending first, then save from what remains, so your plan stays stable over time.

You avoid pushing your budget to the edge. You leave room for bills, food, fuel, and day-to-day costs, which keeps your saving amount realistic and repeatable.

This approach values consistency over speed. Conclusion: steady saving reaches your target date more reliably than aggressive saving that breaks down.

Your target amount and your target date

Your target amount sets the finish line for your saving plan. You decide the figure you want to reach for a deposit or upfront payment, based on the car you want and the monthly payment you aim to keep.

Your target date gives the plan structure. You match your monthly saving amount to a realistic timeframe, so the date works with your income and outgoings, not against them.

Both figures work together.

The numbers we use to estimate your saving plan

We build your saving plan using a small, fixed set of numbers. You provide your monthly saving amount, your target amount, and your start date, which lets us calculate a clear target date without assumptions.

We place household costs first. You factor in rent or mortgage, utilities, food, fuel, and existing finance, then confirm the saving amount that fits around those commitments.

We keep every figure consistent throughout the plan. Stable numbers create a saving plan that stays accurate from the first month to your target date.

Quick calculator: saving amount vs target date

The calculator turns your monthly saving amount into a clear timeline. You enter your saving amount and your target amount, and the calculator shows the number of months required and the month you reach your target.

You can adjust the saving amount and see the result immediately. You raise or lower the monthly figure and watch the target date move, which helps you choose a saving amount that fits your real budget.

The calculator uses the same figures throughout. You get a clear link between what you save each month and the date you reach your target, without confusion or pressure.

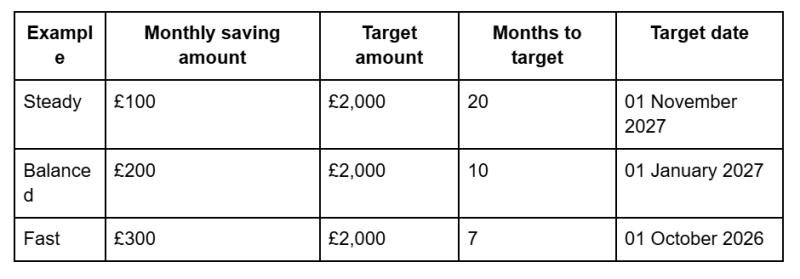

Examples based on common UK budgets

These examples show what your target date looks like with realistic monthly saving amounts. You can use them as a reference point, then swap in your own target amount and monthly saving amount.

Start date: 01 March 2026. Target amount: £2,000. You can copy this format and change the numbers to match your plan.

These figures keep the calculation simple: target amount ÷ monthly saving amount = months to target. You can choose a monthly saving amount that feels comfortable and still get a clear target date.

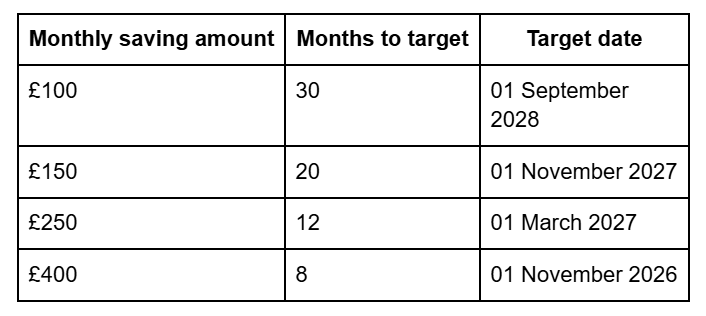

Comparison table: different saving amounts and dates

Your monthly savings amount decides how fast you reach your target. This table shows that link clearly, using the same target amount so you can see the impact of each choice without distraction.

Target amount: £3,000. Start date: 01 March 2026. These figures mirror a common car deposit goal and a realistic starting point.

A lower saving amount keeps monthly pressure low but extends the wait. A higher saving amount brings the date forward but asks for stronger monthly commitment.

The right choice feels sustainable, not forced. You pick the saving amount that fits your life and gives you a target date you can stick to.

What can change your saving plan results

Your saving plan works best when it reflects real life, not fixed assumptions. Changes in income or regular spending can alter your monthly savings amount and shift your target date.

Income changes carry the most weight. A pay rise can increase your saving amount and bring the target date forward, while reduced hours or a job change may require a lower saving amount to keep the plan stable.

Household costs also affect the outcome. Higher energy bills, fuel costs, or childcare can reduce what you save each month, which moves the target date back in a controlled way.

Short-term costs matter too. One-off expenses, like car repairs or annual insurance, may pause or reduce saving for a month, and adjusting the plan early avoids pressure.

The plan stays flexible by design. Reviewing your saving amount protects your budget and keeps your target date realistic.

How your saving plan connects to car finance options

Your saving plan sets the foundation for your car finance options. The target amount you save often becomes your deposit, which directly shapes your monthly payments and lender choice.

A higher deposit reduces the amount you finance. You lower monthly payments and widen the range of car finance options available to you, which gives you more control over the final deal.

A smaller deposit still works with the right structure. You focus on matching the finance term and monthly payment to your budget, not forcing the saving amount higher.

Saving first gives you leverage. A clear saving plan leads to car finance options that fit your budget, not the other way round.

Main image by micheile henderson on Unsplash

Our newsletters emailed directly to you

Our newsletters emailed directly to you